Health insurance in the United States is one of those topics that instantly raises eyebrows—and for good reason. If you’ve ever tried to understand your monthly premium, deductible, or out-of-pocket maximum, you know it can feel like decoding a secret language. At its core, health insurance cost refers to the amount you pay to maintain coverage, including your monthly premium and any additional expenses when you receive care. These costs vary wildly depending on your plan, income, and even where you live.

To break it down simply, there are two major components: premiums and out-of-pocket expenses. Premiums are what you pay each month just to have insurance. Out-of-pocket costs include deductibles, copayments, and coinsurance—basically what you pay when you actually use healthcare services. According to recent data, higher premiums often mean lower out-of-pocket costs and vice versa. So, choosing a plan is a bit like balancing a seesaw—you’re always trading one cost for another.

What makes this even more important today is the rapid rise in healthcare expenses. Nearly half of Americans report struggling to afford healthcare, which highlights just how critical it is to understand these costs. Health insurance isn’t just a financial product—it’s a safety net that can protect you from massive medical bills, but only if you choose wisely.

Definition of Premiums and Out-of-Pocket Costs

Think of premiums as your “subscription fee” for healthcare. You pay it whether you visit a doctor or not. Out-of-pocket costs, on the other hand, are what you pay when you actually need medical attention. These include deductibles (what you pay before insurance kicks in), copays (fixed fees per visit), and coinsurance (a percentage of the bill).

Why Costs Matter More Than Ever

Healthcare costs are rising faster than wages in many cases, putting pressure on individuals and families. With premiums increasing and coverage becoming more complex, understanding your options is no longer optional—it’s essential.

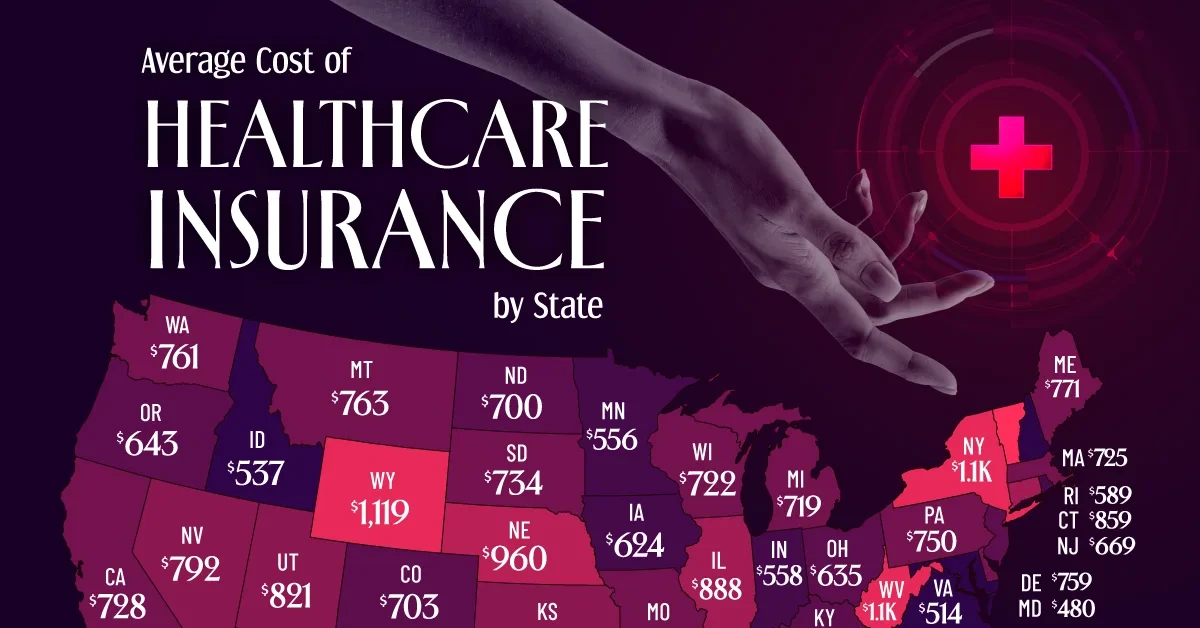

Average Health Insurance Cost in 2025–2026

If you’re wondering, “So how much does health insurance actually cost?”—you’re not alone. The answer depends on several factors, but we can look at national averages to get a realistic picture.

Monthly Premiums for Individuals

In 2025, the average monthly premium for an individual in the Affordable Care Act (ACA) marketplace is around $497 to $590 per month for a standard silver plan. Without subsidies, that number can climb to about $619 or more. For 2026, early estimates suggest premiums are continuing to rise, with some reports showing increases of over 20% in certain regions.

Age plays a huge role here. A 20-year-old might pay around $471 monthly, while someone in their 60s could pay over $1,700 per month. That’s not a small difference—it’s a massive financial shift just based on age alone.

Monthly Premiums for Families

Family plans are where things get really expensive. The average monthly premium for a family in the U.S. is roughly $1,500 to $1,800, depending on coverage and provider. That means families could easily spend over $20,000 per year just on premiums.

To put that into perspective, that’s comparable to buying a new car every year—except instead of a vehicle, you’re purchasing financial protection against medical emergencies. It’s no surprise that many families feel the strain.

Employer-Sponsored Health Insurance Costs

For most Americans, health insurance comes through their employer. While this option is usually cheaper than buying your own plan, the real costs might surprise you.

Average Employer vs Employee Contribution

In 2025, the average total premium for employer-sponsored insurance was about $777 per month for individuals, but employees only paid around $120 monthly, with employers covering the rest. For families, the total premium reached about $2,249 per month, with employees contributing roughly $571.

This system works because employers subsidize a large portion of the cost. Without that support, most people wouldn’t be able to afford coverage at all.

Annual Cost Breakdown

| Coverage Type | Total Annual Cost | Employee Pays | Employer Pays |

|---|---|---|---|

| Individual | $9,325 | ~$1,440 | ~$7,885 |

| Family | $26,993 | ~$6,850 | ~$20,143 |

These numbers highlight something important: even though employees don’t pay the full cost directly, those expenses still impact wages and benefits. Employers often adjust salaries or hiring decisions based on healthcare costs.

ACA Marketplace Insurance Costs

If you’re self-employed or don’t have employer coverage, the ACA marketplace is your main option.

Average Premiums Before Subsidies

Marketplace plans can be pricey without financial help. The average cost is around $590 per month, but it can exceed $1,000 depending on the plan tier and location. Bronze plans are cheaper, while platinum plans offer more coverage at a higher cost.

Costs After Subsidies

Here’s where things get interesting. About 90%+ of ACA enrollees receive subsidies, which significantly reduce monthly premiums. In many cases, people pay far less than the listed price—sometimes even under $100 per month.

Subsidies are based on income, which means two people choosing the same plan could pay completely different amounts. It’s a bit like airline pricing—what you pay depends on your situation.

Medicare and Government Programs

Medicare Costs Overview

The Medicare is primarily for people aged 65 and older. While some parts are free (like Part A for hospital coverage), others require monthly premiums. These costs vary depending on income and coverage choices.

Medicaid and Low-Income Options

Medicaid provides free or low-cost coverage for those with limited income. Eligibility varies by state, but it remains one of the most important safety nets in the U.S. healthcare system.

Key Factors That Affect Health Insurance Costs

Age and Location

Older individuals typically pay higher premiums because they’re more likely to need medical care. Location also matters because healthcare costs vary by state and even by city.

Plan Type and Metal Tier

Plans are categorized into Bronze, Silver, Gold, and Platinum tiers. Bronze plans have lower premiums but higher out-of-pocket costs, while Platinum plans are the opposite.

Lifestyle and Health Conditions

Smoking, chronic illnesses, and overall health can significantly impact your premiums. Insurers assess risk, and higher risk usually means higher costs.

Why Health Insurance Costs Are Rising

Medical Inflation and Drug Prices

The cost of medical services and prescription drugs continues to rise. New treatments and technologies, while beneficial, often come with high price tags.

Demand for Healthcare Services

An aging population and increased use of healthcare services are driving costs upward. More people are seeking treatment, which puts pressure on the system.

How to Reduce Health Insurance Costs

Using Subsidies and Tax Credits

If you qualify, subsidies can dramatically reduce your monthly premium. Always check your eligibility—it could save you hundreds of dollars.

Choosing the Right Plan

Selecting the right balance between premium and out-of-pocket costs is key. If you rarely visit the doctor, a high-deductible plan might save you money. If you need frequent care, a higher premium plan could be worth it.

Conclusion

Health insurance in the United States is complex, expensive, and constantly evolving. From employer-sponsored plans to ACA marketplace options, the costs vary widely based on your situation. On average, individuals can expect to pay around $500–$600 per month, while families may face premiums exceeding $1,500 monthly. Add in deductibles and other expenses, and the total cost can quickly climb.

Understanding how these costs work—and what factors influence them—can help you make smarter decisions. Whether it’s choosing the right plan, taking advantage of subsidies, or simply budgeting more effectively, being informed is your best defense against rising healthcare expenses.

FAQs

1. What is the average health insurance cost per month in the USA?

The average monthly cost ranges from $497 to $590 for individuals, while family plans can exceed $1,500 per month.

2. Why is health insurance so expensive in the US?

Costs are driven by medical inflation, high drug prices, and increased demand for healthcare services.

3. Is employer health insurance cheaper?

Yes, because employers typically cover a large portion of the premium, reducing the employee’s cost.

4. Can I get health insurance for free in the USA?

Some people qualify for Medicaid or heavily subsidized ACA plans, which can reduce costs significantly.

5. How can I lower my health insurance premium?

You can lower costs by qualifying for subsidies, choosing a higher deductible plan, or comparing multiple providers.